When People Start Saying 'Index Funds Aren't Enough,' AI Stocks Are Probably Overheated

My friend just made $20K on Micron. Social media is full of people comparing index funds to AI funds over four-week windows. Here's why I'm not changing a thing.

Table of Contents

- Quick Japan context: what I actually hold

- My friend made $20K. I said “nice.” That was it.

- Three signals I’m seeing in June 2026

- Why I’m not buying individual AI or semi names — even now

- The single best thing about mutual funds is the part nobody talks about

- Doing nothing is harder than it sounds

- The actual risk isn’t the AI bubble. It’s the timeframe collapse.

- What I’m not claiming

- What I’m going to do tomorrow morning

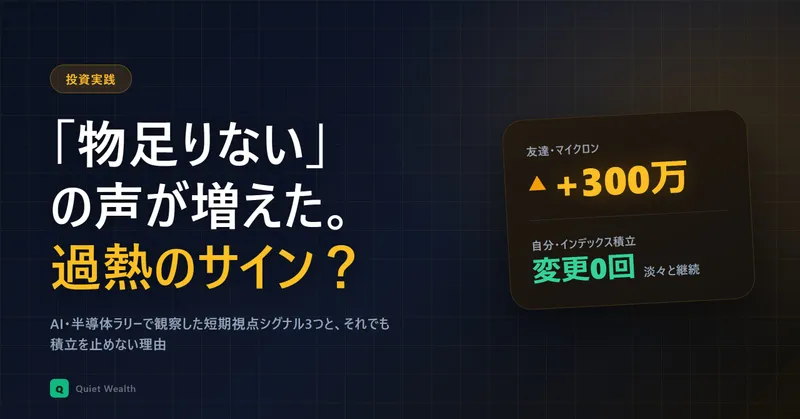

A friend of mine just made about ¥3 million on Micron. That’s roughly $20,000 in a few weeks.

He told me over text, half-bragging, half-checking if I’d jumped in too. I hadn’t. I didn’t even feel jealous, which surprised me a little. I just thought: he’s all the way in on the AI trade now.

And then I thought something else, which is what this post is about: when my non-investing friends start sending me screenshots of semiconductor gains, and when half the personal-finance posts in my feed are titled some version of “index funds aren’t enough anymore,” that’s not noise. That’s a data point.

I’m 46. IT security sales in Tokyo, dual-income household, mid-$300K portfolio (roughly ¥50M+). I’ve been buying the same three funds on autopilot for years. I’ve been here before — different boom, same shape of crowd — and I’m writing this mostly to remind myself what to do, which is, basically, nothing.

Quick Japan context: what I actually hold

Before I go further, two terms English-speaking readers don’t usually know:

- Oruka-n (オルカン) — Japanese shorthand for a low-cost global all-cap index fund, roughly equivalent to a total world stock ETF like VT or ACWI. It’s become the default “boring” answer for Japanese index investors over the last few years.

- FANG+ — a Japanese-popular index of ten US tech megacaps. NVIDIA, Microsoft, Apple, Alphabet, Amazon, Meta, Broadcom, Netflix, ServiceNow, Crowdstrike (it shuffles). Think Magnificent 7 plus a couple of seasoning picks. Equal-weighted, rebalanced quarterly.

I hold three funds: FANG+, Nasdaq-100, and global all-cap. That’s it. I wrote about why in why these three funds, so I won’t relitigate the whole thing here.

The relevant part for today is: I already have more concentrated AI and semiconductor exposure than most people realize, and I didn’t buy a single individual chip name to get it.

My friend made $20K. I said “nice.” That was it.

He’s a good friend. He’s not an idiot. He got in on Micron at what turned out to be a great moment, and he was right. Good for him, genuinely.

But I noticed what didn’t happen inside me when I heard the number. No “I should’ve bought too.” No quiet stomach-tightening. No mental math of “if I’d put ¥5M in, that’d be…” I’ve felt that feeling plenty of times in my life. I know what it looks like from the inside. This wasn’t it.

What I felt instead was something closer to recognition. Like — oh, we’re in that part of the cycle again.

Chasing a hot name means you have to be right twice. Buy-right and sell-right. Most people, including past versions of me, are good at one and terrible at the other. I sold three stocks in 2010 that would be worth roughly ¥30 million today if I’d just shut up and held them. I wrote that one out in painful detail in the three stocks I sold for ¥30M of regret. After that, I just stopped touching individual names. Eight years of index-only and counting.

Here’s the part I find weirdly comforting about my friend’s win, though. He’s going to have to decide when to sell. Not “eventually.” He’s going to have to decide every single day until he does. Every green candle is going to whisper “let it ride.” Every red candle is going to whisper “lock it in.” The next time chip prices wobble for some reason that has nothing to do with Micron, he’s going to be sitting there at 11pm doing the same mental calculation tens of thousands of other Micron holders are doing at the same time. Whatever decision he makes will be the wrong one for half of them. That’s just how individual stocks work in a crowded trade.

I do not have to do any of that. The fund decides. I’d rather give up the upside than rent that headspace.

So I texted him “nice, congrats” and meant it. Then I closed the app.

Three signals I’m seeing in June 2026

I trust crowd vibes more than price charts. Price tells you what just happened. Crowd behavior sometimes tells you what’s about to.

Here are three things I keep noticing this month. None of them is a sell signal. Together, they’re a temperature reading.

Signal 1: People are bragging about short-term yen figures, not annualized returns

A year ago, the typical investing post in Japanese X looked like “+38% over 6 years, here’s my contribution pace.”

Now it’s ”+¥3M in three weeks on Micron.” “+50% in a month on a semi ETF.” Specific stock, specific window, raw yen amount.

Annualized returns disappeared. Time horizons collapsed. The unit of measurement quietly shifted from “compounding over a decade” to “headline gain since last paycheck.”

Other people’s profits aren’t my business. But the shape of how people talk about profits — that’s a market reading. When the unit shrinks from years to weeks, you’re seeing the timeframe of the marginal buyer.

The marginal buyer is the person who decides the next price. If the marginal buyer’s holding period is six weeks, you’re not really in an “AI long-term thesis” market anymore. You’re in a momentum market wearing a thesis costume. Those can run a long time, sometimes a wildly long time, but the eventual unwind isn’t about whether AI is real. It’s about whether the next person in line has a six-week clock too. At some point the line gets shorter and prices have to find people with a longer clock again, and that handoff is rarely smooth.

Signal 2: People are benchmarking global index funds against AI funds over four weeks

This one is the one that actually makes me wince a little.

“Global all-cap returned +3% last month. The AI-themed fund returned +18%. Why am I even in the boring stuff?”

Read that sentence carefully. The person isn’t necessarily wrong about the numbers. They’re wrong about the timeframe. A global all-cap index fund is something you evaluate over 10, 20, 30 years. Holding it up against a sector fund over four weeks isn’t analysis; it’s regret-sampling.

The collapse of the comparison window is the tell. Once your brain starts measuring index funds on a monthly P&L, your brain has already left index-fund mode. You’re a stock picker now. You just don’t know it yet.

And the worst part — I say this as someone who’s done it — is that the comparison feels rigorous. It feels like the responsible thing. You’re “running the numbers.” You’re “looking at performance.” Both funds are real, both numbers are real. What’s missing is that the units don’t match. You’re comparing thirty-year compounding to four-week sentiment and treating them like the same kind of object. That’s not analysis. That’s the moment you stop being a long-term investor without noticing.

Signal 3: “Index funds aren’t enough anymore”

This is the loudest one, and the one that gave this article its title.

It comes from people who used to defend index funds. Not the day-traders — those guys always thought index funds were boring. This is the previously-patient crowd. The ones who’d post Bogle quotes a year ago. They’re now saying things like, “Index returns feel slow,” or “I want something more aggressive.”

Slow compared to what, exactly? Slow compared to a sector that just ripped face for nine months straight.

Here’s the part that actually matters: when a three-out-of-ten-years rally makes index returns feel “slow,” your nervous system has adjusted to the boom as the new normal. That’s not a market view. That’s calibration drift. And historically, calibration drift in the patient crowd is one of the last things that happens before things stop working.

I’m not predicting a top. I have no idea where the top is. I’m saying: when the patient money starts complaining the boring thing is too boring, the boring thing is usually about to look great again, on a long enough delay to ruin most people’s resolve.

Why I’m not buying individual AI or semi names — even now

The natural follow-up: “Okay, if you think it’s overheating, are you trimming?”

No. And I’m not buying chip stocks either. I’m doing exactly what I did last month, and the month before, and the month before that.

The math, honestly, is boring. Inside FANG+, four of the ten names are direct AI infrastructure plays. Nasdaq-100 holds basically every name a thematic AI fund would hold, weighted by market cap, which mechanically means more weight on the winners. Even the global all-cap fund has the US megacaps in its top holdings.

I added it up once. The portion of my portfolio that’s effectively riding the AI/semiconductor trade is meaningfully bigger than people assume when they hear “he’s just an index guy.”

So when someone asks if I’m worried about missing the AI move, I think — I’m not missing it. I just got there by a different door. The door where I don’t have to decide when to leave.

I’ve written about the “am I actually paying for this product” filter I use to sanity-check the AI story in the AI hype filter I actually use. Short version: I pay for AI every month, and have for almost a year. Whether the trade is overheated and whether AI is real are two different questions, and I think the answer to the second one is yes.

The single best thing about mutual funds is the part nobody talks about

If you ask people what’s good about index funds, you’ll get the usual list. Low cost. Diversification. Tax efficiency. All true. All boring. None of it is what I’d actually put first.

The thing I’d put first is this: the fund rebalances the holdings for me. Forever. Automatically. Per a public rulebook.

Companies that grow get added. Companies that shrink get dropped. The Nasdaq-100 reconstitutes annually. FANG+ reshuffles quarterly. Global all-cap funds rebalance on schedule. I have never once made a decision about which stock should be in or out of my portfolio.

Think about what that actually saves. To run a concentrated AI portfolio yourself, you’d have to: read every quarterly earnings call for ten companies, track competitive moats, model out cap-ex cycles, watch foreign exchange, watch interest rates, listen for downgrade rumors, and decide — for each name, every quarter — whether today is the day to add, hold, or sell. And you’d still get the timing wrong sometimes, because everyone does.

I tried that for years in my late 20s and early 30s. I was not good at it. I don’t think most retail investors are good at it. Eight years ago I outsourced the whole decision tree to a rulebook, and I’ve slept better ever since. The exact mental shift is in how I learned to stop thinking and just hold the index.

The fund’s job is to swap winners in and losers out without asking me. My job is to keep funding it.

Quick concrete example, because the abstract version sounds too clean. Five years ago, the dominant chip name everyone was excited about wasn’t NVIDIA. Intel was still being treated as the obvious infrastructure play. NVIDIA was a graphics company that gamers liked. If I had built a “concentrated AI bet” portfolio in 2020 based on consensus at the time, I would have weighted Intel heavier than NVIDIA. I would have been spectacularly wrong, and I’d have spent the last three years either holding a loser, selling at the wrong time, or rotating in late after NVIDIA had already done most of the run. The fund did none of that. The fund just let position sizes adjust as the prices changed, which is the same thing the smartest active managers in the world try to do and fail at on average. The fund doesn’t have an ego. That’s a real edge.

Doing nothing is harder than it sounds

“Do nothing” sounds passive. It is not.

Right now, on any given weekday: a friend texts about Micron. My X feed has three AI-fund screenshots in the first scroll. A financial newsletter I subscribe to opens with “is it time to rotate?” The 4am market podcast I sometimes catch is debating whether semiconductors are 30% overvalued or just getting started. The dopamine pull to do something — anything — is real and constant.

What actually works for me is a reframe.

I stopped reading other people’s wins as “you should’ve gotten in.” I started reading them as data points about market temperature. The friend who made $20K on Micron isn’t a chance I missed. He’s the heat gauge. Three friends like him in a month? Heat gauge climbing. Patient investors saying “index isn’t enough”? Heat gauge climbing more.

The reframe matters because it gives my brain something to do with the information without turning it into a trade. The gauge goes up. I write it down. I notice. I keep buying. The information becomes observation instead of pressure.

Higher temperature, lower trading. That’s the rule. Because in the version of me from fifteen years ago, higher temperature meant more activity, and more activity meant ten new ways to be wrong.

I also limit how much input I let in. I don’t have notifications on for any brokerage app. I don’t follow accounts whose entire feed is daily P&L screenshots. I read company earnings if I’m curious, not because I’m planning to act on them. And when a friend texts me about a hot stock, I read the message once, write something genuine back, and move on. The information enters; the impulse to trade does not. That’s an active discipline, not a passive one. It looks lazy from the outside. From the inside, it’s the most expensive habit I’ve ever built.

The actual risk isn’t the AI bubble. It’s the timeframe collapse.

Honestly, this is the part I keep coming back to.

Whether AI stocks are 20% overvalued or 50% or fairly priced — I genuinely don’t know, and I don’t need to. My monthly contribution doesn’t care. The funds rebalance regardless of my opinion.

The thing that would actually hurt me isn’t a 40% drawdown in semiconductors. I’ve sat through worse. What would hurt me is letting the crowd’s timeframe become my timeframe.

The moment I hear “Micron, $20K, three weeks” and start running the math on what I could have made — what window I could have caught — what name I should be looking at next — that’s the start of the collapse. From there it’s a short walk back to the version of me that sold those three stocks in 2010 and spent fifteen years explaining it to myself.

A timeframe collapse is invisible while it’s happening. You don’t notice you’ve shrunk from “decades” to “months” to “weeks.” You just notice you’ve started checking your account more, and feeling worse, and trading more, and feeling worse, and one day you wake up and the system you built is gone. Rebuilding the system takes years. I’m not exaggerating. It took me roughly the second half of my 30s.

So the discipline I’m actually practicing right now is not “don’t buy Micron.” That part’s easy. It’s: don’t let my mental clock get faster than the funds’ rebalance schedule.

What I’m not claiming

To be clear about what this article isn’t.

I’m not calling a top. I have no idea where the top is, and the people who think they do are almost always the same people who called the last three tops, two of which didn’t happen and one of which they sold into early. I’ve watched this game my whole adult life. Nobody has a clean record.

I’m not saying AI is a bubble. I think the underlying technology is real, I pay for it every month, I use it every day, and I’d bet the next decade of productivity gains skews toward companies that figure out how to deploy it. The trade and the technology are two different questions. A real technology can be in an overheated trade. Internet stocks in 1999 were both a real technology and a bubble. The internet won. Most of the 1999 stocks lost. Both things were true.

I’m not telling anyone else to do nothing. If you want to bet on Micron, that’s your call. I don’t think it’s a great asymmetric bet right now, but I’ve been wrong before. The thing I’m allergic to isn’t taking risk. It’s pretending the risk has been removed because the recent past has been kind.

What I am saying is narrower than any of those. I’m saying: when the patient money starts measuring itself against impatient money on impatient money’s timeframe, something is off in the patient money. The discipline that survived the last drawdown is the discipline being tested right now, and most of the testing happens in the form of social pressure, not market pressure.

That’s it. That’s all this is.

What I’m going to do tomorrow morning

Nothing different.

The monthly contribution will hit on its usual day. It will buy FANG+, Nasdaq-100, and global all-cap in the same ratios it has for years. I will open the brokerage app, see the buy went through, close the app. That is the entire ritual.

The market is overheating. I think it probably is. I have no idea if “overheating” lasts another six weeks or another six quarters before something gives. Some past booms ran way longer than the patient crowd thought possible. Some broke earlier. Trying to call the turn was never my edge, and it isn’t now.

My edge is the same edge it’s been for eight years: a rulebook that doesn’t need my opinion to keep running. The less I have to decide, the more I get to keep.

So I’m going to do what the observer does. Watch the heat gauge. Don’t touch the dials. Let the friends, the screenshots, the “index isn’t enough” posts roll past. Note them. Keep buying.

If you’re reading this and feeling the pull — the gain envy, the “maybe just this once,” the screenshot-induced regret math — I get it. I’m not above it. The defense isn’t willpower. The defense is a system that runs whether you feel like it or not.

That’s it. That’s the whole strategy. Boring on purpose.

Nothing here is investment advice. I’m a guy with a portfolio writing about how I think about it. Your situation, tax setup, and timeline are not mine.

Related Articles

I Sold 3 Japanese Stocks 15 Years Ago. They'd Now Be Worth $200K More — Here's What I Got Wrong

A 46-year-old Tokyo salaryman walks through three stock sales from 2011 that turned into a $200K opportunity cost — and what finally fixed the pattern.

Holding $260K in Unhedged Dollar-Denominated Funds in Japan: Why I Never Used Currency Hedging

A Japan-resident investor's case for unhedged USD funds: why I chose unhedged over hedged versions (fees + DCA fit), what ¥159 USD/JPY means for my ~$260K portfolio, and why I won't sell or stop contributions even if the yen strengthens.

I Owe $170K on My Mortgage at 0.6% Interest. Here's Why I Won't Pay It Off Early

With a 0.6% variable-rate mortgage in Japan, should I prepay or keep investing in index funds? Eight years of real decisions, including getting rejected for mortgage insurance because of a therapy visit.